VAT and CCL

Frequently Asked Questions

VAT and CCL explained

Find out about the rates that VAT and CCL are chargeable on electricity and gas supplies with our guide

- Residential - Small Business Customers

- Charities

- Third Party Intermediaries

- Other Intermediaries

- Renewable Energy

- Supplies to Electricity Producers

- Other Uses Qualifying for Exemption

- High Energy Usage

- General

I’m a residential (domestic) customer and would like to understand how VAT & CCL applies to me

Domestic use of energy qualifies for reduced rate of VAT, which is currently at 5%. CCL isn't charged on any domestic use of energy.

My energy supply is for accommodation but isn't a house/flat. Does the same rule apply?

Domestic use doesn't only cover dwellings, it also includes certain types of residential accommodation (excluding hospitals, prisons or similar institutions, hotels or similar establishments).

Examples:

Armed forces residential accommodation

Caravans

Children’s homes

Homes providing care for elderly/disabled, dependence on alcohol/drugs or people with mental disorder

Houseboats

Hospices

Monasteries, nunneries and similar religious communities

School and university residential accommodation for students or pupils

Self-catering holiday accommodation

I’m a business customer, but use small amounts energy. Do I benefit from a reduction in VAT & CCL?

Yes, businesses which use small amounts of energy are classed as “de minimis”. You'll fall under domestic use, even when the supply is to a business customer. This means that they will automatically be subject to VAT at 5% and will be excluded from CCL (no requirement to produce a certificate).

What does “de minimis” mean?

The following rules apply to each premises. Please note that we are required to take into the account of all meters on one premises when determining whether or not the de minimis rules should be applied.

Electricity | Gas |

De minimis means supplies of not more than an average rate of 33 kWh per day (1,000 kWh per month) of electricity at one premises are subject to VAT at the reduced rate. | De minimis means supplies of not more than an average rate of 5 therms or 145 kWh per day (150 therms or 4,397 kWh per month) of piped gas at one premises are subject to VAT at the reduced rate. |

The de minimis calculation is applied by looking at the average unit consumption for each individual billing period and as such, it is possible to be de minimis in some periods and not others.

The premises are used partly for residential accommodation and partly for business purposes. What rate of VAT should apply?

If the premises are used for a mixture of business purposes and residential accommodation then the VAT and CCL would be apportioned between the two (i.e. reduced rate for the portion that qualifies and standard rate for the rest). If more than 60% of the energy relates to the accommodation element then the whole supply is subject to VAT at the reduced rate (and excluded from CCL).

In order to obtain this relief, you must send a completed VAT certificate to us.

Please note - Acceptance of this form automatically results in a proportionate reduction in the CCL that you pay.

Residential - Small Business Customers

I’m a residential (domestic) customer and would like to understand how VAT & CCL applies to me

Domestic use of energy qualifies for reduced rate of VAT, which is currently at 5%. CCL isn't charged on any domestic use of energy.

My energy supply is for accommodation but isn't a house/flat. Does the same rule apply?

Domestic use doesn't only cover dwellings, it also includes certain types of residential accommodation (excluding hospitals, prisons or similar institutions, hotels or similar establishments).

Examples:

Armed forces residential accommodation

Caravans

Children’s homes

Homes providing care for elderly/disabled, dependence on alcohol/drugs or people with mental disorder

Houseboats

Hospices

Monasteries, nunneries and similar religious communities

School and university residential accommodation for students or pupils

Self-catering holiday accommodation

I’m a business customer, but use small amounts energy. Do I benefit from a reduction in VAT & CCL?

Yes, businesses which use small amounts of energy are classed as “de minimis”. You'll fall under domestic use, even when the supply is to a business customer. This means that they will automatically be subject to VAT at 5% and will be excluded from CCL (no requirement to produce a certificate).

What does “de minimis” mean?

The following rules apply to each premises. Please note that we are required to take into the account of all meters on one premises when determining whether or not the de minimis rules should be applied.

| Electricity | Gas |

| De minimis means supplies of not more than an average rate of 33 kWh per day (1,000 kWh per month) of electricity at one premises are subject to VAT at the reduced rate. | De minimis means supplies of not more than an average rate of 5 therms or 145 kWh per day (150 therms or 4,397 kWh per month) of piped gas at one premises are subject to VAT at the reduced rate. |

The de minimis calculation is applied by looking at the average unit consumption for each individual billing period and as such, it is possible to be de minimis in some periods and not others.

The premises are used partly for residential accommodation and partly for business purposes. What rate of VAT should apply?

If the premises are used for a mixture of business purposes and residential accommodation then the VAT and CCL would be apportioned between the two (i.e. reduced rate for the portion that qualifies and standard rate for the rest). If more than 60% of the energy relates to the accommodation element then the whole supply is subject to VAT at the reduced rate (and excluded from CCL).

In order to obtain this relief, you must send a completed VAT certificate to us.

Please note - Acceptance of this form automatically results in a proportionate reduction in the CCL that you pay.

Why does my invoice show a charge for the Climate Change Levy (CCL) and what is it for?

Climate Change Levy (CCL) is a UK government tax imposed on certain supplies of energy (primarily electricity, gas, coal, coal products and LPG).

Energy suppliers are required to collect the levy on behalf of HM Revenue and Customs. EDF acts purely as a tax collector and makes no money from the levy.

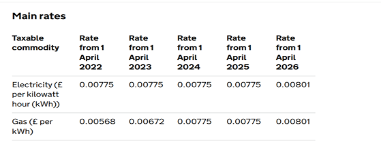

What are the CCL charges?

Charities

I manage the accounts for a registered charity and understand that I might be able to receive my energy bills VAT & CCL free. Is this correct?

No, but if the premises are used only for charitable non-business purposes then the reduced rate of VAT would apply. If the premises are for a mixture of business and non-business use then it is possible to split the charges between business (20% Standard Rate VAT) and non-business (5% Reduced Rate of VAT).

If more than 60% of the energy relates to the non-business element then the whole supply is subject to VAT at the reduced rate (and excluded from CCL).

In order to obtain this relief, you must send a completed VAT certificate to us.

Note, completion of this form automatically results in a proportionate reduction in the CCL that you pay.

What does “non-business” mean?

This is a complex point and detailed guidance can be found in the HMRC leaflet (Notice 701/1) that is designed for charities.There are a couple of points which are worth highlighting:

An organisation that is run on a not-for-profit basis may still be regarded as carrying on a business activity for VAT purposes.

Where a charity charges for their goods or services, HMRC see it as ‘business’ income which doesn’t qualify, i.e.

- Sale of goods (e.g. charity shops)

- Hiring out the premises (e.g. village hall)

- Charging for admission (e.g. community or leisure centre)

- Fee-paying schools

If the charity makes no charge at all the activity is unlikely to be considered business.

Can you confirm whether or not my charity is making non-business supplies?

Unfortunately this is not something that we can advise you of. Detailed guidance can be found in the HMRC leaflet (Notice 701/1) that is designed for charities.If you are unsure how the VAT rules apply to you, please either contact HMRC or your tax advisors.

Does a Community Amateur Sports Centre (CASC) qualify for the relief?

No, unfortunately, this relief only applies to registered charities.