Keeping a role for the market: how Reformed National Pricing can help deliver lower system costs

It is now four years since the Review of Electricity Market Arrangements (REMA) process commenced in July 2022, at a time of very high electricity prices caused by Russia’s invasion of Ukraine. Over time the scope of REMA, which had started with a very broad remit, narrowed considerably to what became an intense and relatively polarising sector wide debate on the case for zonal pricing.

A year ago, the government decided against introducing zonal pricing. The focus of discussion has now moved to how we can deliver a more efficient electricity system under a national pricing model, combined with strategic system planning. This is what government now refers to as Reformed National Pricing (RNP).

As with the previous REMA exercise, the scope of RNP encompasses both questions of investment signals (how to ensure electricity investment is of the right scale and in the right places) and operational market dynamics (how to ensure electricity markets operate efficiently on a daily and real-time basis). At the heart of these questions are choices about the role of markets vs central planning in the future electricity system, and what market signals (e.g. via network charging) projects should be exposed to, both at the development and operational stages.

Recent publications by DESNZ, Ofgem and NESO have started to flesh out options for reform. But four years on from the start of the REMA process, and with high British electricity prices a concern once again, decisions are needed on how the future market framework will operate. The critical importance of affordable energy prices to households and the rest of the British economy means it is essential those decisions target the least cost power system achievable. Lower cost electricity will also support electrification and thus wider government objectives around energy security and decarbonisation.

In this blog we set out EDF’s view on the key issues and how the right RNP decisions can help deliver a lower cost electricity system over the long-term.1

In this article:

- What is the role of strategic planning in the future electricity system?

- What is the role for locational network charging?

- Making a national electricity market work better

- Conclusion

- FAQs

What is the role of strategic planning in the future electricity system?

The first key question raised by the RNP programme is the role that the Strategic Spatial Energy Plan (SSEP), being developed by NESO, should play in the future electricity system. SSEP will reach a view on the optimal build-out of a large ongoing programme of new generation and network construction across the country – broadly estimated to require around £20bn of new investment per annum out to 2050.2

At EDF, we recognise that strategic planning can play a valuable role in helping to shape the future electricity system. Decisions about what gets built where make big differences, and for options like wind, the SSEP needs to consider both the wind resource at different locations and the costs of transporting wind power around the country. The objective should be to target the lowest cost electricity system over the long-term, with realistic assessment of potential demand trends and scenarios. The scale and pace of future investment in the electricity system also creates a clear case for better co-ordination of generation and network build. The growth in constraint costs we have witnessed in recent years illustrates the problems that arise when this co-ordination is lacking.3

But while our past approach may have lacked a useful element of strategic planning, there are still big decisions to take on how far down this road to go - how directive the SSEP should be and what levers are used to implement it. EDF believes there is a balance to be struck between high-level guidance from the plan and allowing markets to shape the final outcome. We do not favour an overly prescriptive approach.

The SSEP will inevitably have some limitations – it is a function of the assumptions it makes about future demand and technology costs. That future is clearly uncertain and no central planner can accurately predict all the drivers of system value long into the future, nor understand in detail all the factors which will determine the most cost-effective projects to build. We know that past assumptions have often been proven wrong in practice.

For these reasons, we think that allowing markets to optimise around a broader plan is likely to deliver the best outcome for consumers. The RNP framework needs to have flexibility to adapt to changing circumstances. Competition between projects and technologies, responding to constantly evolving market prices and signals over time, helps identify the best projects in the best locations. Facilitating competition means allowing for project attrition: recognising and explicitly planning for the reality that not all development projects will ultimately be built. This in turn requires flexibility in the overall national plan and the target levels of generation build by technology in different parts of the country.

In summary, allowing markets to still play a key role in determining the final mix of generation and its locations across the country will ultimately deliver the best outcome for consumers. This is particularly important for those options such as wind (onshore and offshore), solar and storage, where multiple project options and potential locations exist.

What is the role for locational network charging?

The next key question to be answered in the RNP programme is the role of network charging in sending locational investment signals. DESNZ’s consultation includes a range of approaches on this issue, with some involving no or only a limited role for locational network charges. The argument has been made that since the SSEP will reach a view on generation locations and the right level of supporting network build, there is no clear ongoing role for a locational network charge.

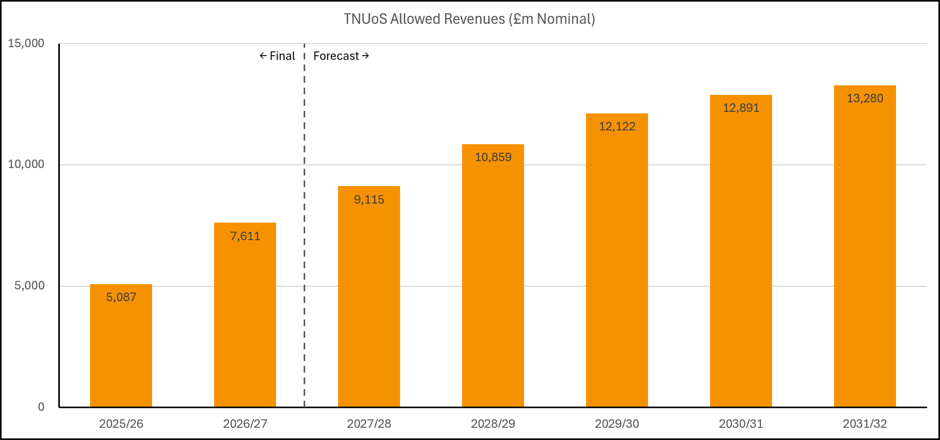

Network costs already make up a large proportion of electricity system costs, and they are rising substantially. Electricity transmission investment is expected to increase nearly fourfold to £70 billion in the latest price control period (RIIO-ET3). The chart below shows the forecast increases in transmission revenues driven by this increasing investment. As a result, transmission network costs for domestic customers have increased by £66 per annum under the price cap. This increase has offset much of the benefit of the government’s recent decision to take some policy charges off domestic bills.4

In the broader context of high British electricity prices, it is imperative that we are building the right amount of network, in the right places, but no more than this. More scrutiny is needed by NESO and Ofgem of the future network investment programme to establish whether the existing network build programme meets this test. We plan to say more about that question in a forthcoming blog.

In EDF’s view, another key part of a policy mix to make sure network build is appropriate over the long-term is to ensure that individual generation projects and technologies continue to be exposed to the relative network costs and benefits that they bring with them. To be as efficient as possible, these market signals should be cost reflective.

This is the role that locational transmission network charging (TNUoS) can play. Cost reflective network charging can be applied in a consistent and transparent way, irrespective of the technology or location of generation, or whether it is expected to operate within or outside a government support scheme. It can provide a market-based signal which will help ensure competitive processes and market dynamics factor in all relevant costs to consumers - and thus help deliver a least cost electricity system in practice.

Some argue that network charges have become too complex and uncertain to perform this function, and they are now too difficult and controversial to reform. We disagree.

Certainly, the current charging approach needs urgent improvement to deliver much more predictability for developers, at a suitably early stage of project development. These changes will facilitate lower project risk premia and deliver lower costs for consumers. Network charges should also reflect the network we plan to build, not just the network we have today. But these reforms are eminently deliverable, given the visibility of future network plans that should come from the strategic planning process and the right steer from government on the outcomes it wants to see.

Predictability should also be provided in the coming months for bidders into AR8, and other projects close to investment decisions, on the network charges that will apply for these developments. Without such certainty, additional un-necessary risk premia costs will be priced into Contracts for Difference (CfD) bids, and consumers will be locked into bearing those extra costs, amounting to many £bn, over the life of the CfD scheme.

Making a national electricity market work better

Alongside the big picture questions around the nature of the SSEP and how it feeds through into investment decisions, there are also decisions to be taken on how best to operate the market to reduce costs and improve efficiency. DESNZ’s RNP Delivery Plan focusses here on measures to improve the operation of the Balancing Mechanism (BM) and to reduce the volume and cost of existing electricity system constraints. Although not formally part of the RNP programme, efforts to ensure improved electricity trading with the EU across interconnectors, and consistent carbon pricing across UK and EU electricity markets, could also be seen as an important part of these efforts.

EDF recognises the need for changes to improve market operations and reduce constraint costs. We favour changes to the BM to increase participation of smaller assets and consider this will help address many of the current issues the system operator is facing. On constraints we joined with other companies in supporting LCP Delta to highlight a range of ways in which constraint costs can be reduced over the remainder of this decade.5 This work highlighted the potential to reduce costs by up to several £bn per annum. It is encouraging that DESNZ Delivery Plan recognises many of these same options. We would like to see further ambition by NESO, Ofgem and government to help stem the growth in constraint costs as much as possible, including looking more closely at options to procure gas turn-up generation earlier in time.

Conclusion

The next step in Reformed National Pricing will involve key decisions about the future shape of the GB electricity system. With debates about zonal pricing having consumed much industry and government focus over the past few years, timely decisions by government are now needed to deliver real progress.

At the heart of these decisions is a judgement to be made about the right balance to be struck between central planning via the SSEP and competition and market signals in determining the generation mix and its locations. Getting this balance right will be critical, and EDF believes that retaining some flexibility in the plan and an important role for the market in delivering this new framework, while exposing generators to the different network costs they bring, will serve the best interests of consumers over the long-term.

Reformed National Pricing FAQs

What is Reformed National Pricing?

Reformed National Pricing is the UK Government’s preferred electricity market reform model under REMA. It retains a single national wholesale electricity price across Great Britain while introducing targeted reforms to improve system efficiency, strengthen investment signals and reduce network constraints. The aim is to deliver a more secure, affordable and decarbonised power system without moving to a regional or zonal pricing model.

What is the Electricity Market Arrangements (REMA) process

The Review of Electricity Market Arrangements (REMA) is the UK Government’s programme to reform electricity market rules so they support a secure, affordable and decarbonised power system. Launched in 2022, REMA has examined how wholesale electricity markets should evolve to deliver net zero at lowest cost to consumers, culminating in a decision to retain a national electricity market while introducing targeted reforms through a Reformed National Pricing approach.

What is the Strategic Spatial Energy Plan?

The Strategic Spatial Energy Plan (SSEP) is a long-term plan being developed by the National Energy System Operator (NESO) to identify the optimal locations, technologies and timing for future energy infrastructure across Great Britain. Focusing initially on electricity and hydrogen generation and storage, the SSEP is intended to guide network investment and support a more coordinated, cost-effective transition to a secure, decarbonised energy system.

Find out more:

- How we’re helping our customers who are most in need

- Energy bill support

- How EDF are building An Electric Britain

- For EDF’s wider views on electricity prices and what can be done to reduce them, see our blog: UK energy debt: why the crisis is deepening and what must change

- Based on the CCC’s 2019 Net Zero analysis. Investment needed to achieve a clean power system by 2030 has been estimated by NESO to be around £40bn per annum.

- We have also published some recent views on constraint costs

- Further network cost increases from distribution level price controls, operating to a different timeline, are also possible

- https://www.lcp.com/en/insights/publications/cutting-gb-grid-constraint-costs-what-reformed-national-pricing-could-achieve-by-2030

Related articles

UK energy debt: why the crisis is deepening and what must change

The Warm Homes Plan: why faster delivery is critical for consumer bills and the country’s energy security