Rising energy bills: Can anything be done? Absolutely.

Over recent weeks, the cost of energy and the impact on household bills have been making headlines. This is perhaps unsurprising as we approach the point in the year where people are turning on their heating and bills remain c. 40% above pre-crisis levels1. As a supplier we are seeing first-hand the challenge facing consumers, with energy debts reaching record levels, further driving up bills for all. Debt-related costs are already costing every household on average c. £60 a year.

Part of the challenge is that the country is not in charge of its own destiny when it comes to energy prices. Global events have taught us that the importance of investing in energy security cannot be overlooked as we remain exposed to price volatility in the global market for imported energy, such as oil and gas.

Building homegrown sources of energy is crucial to improving our energy security and better insulating ourselves from large swings in international energy prices. If Hinkley Point C had been operating during the energy crisis, it would have saved £4billion on bills.

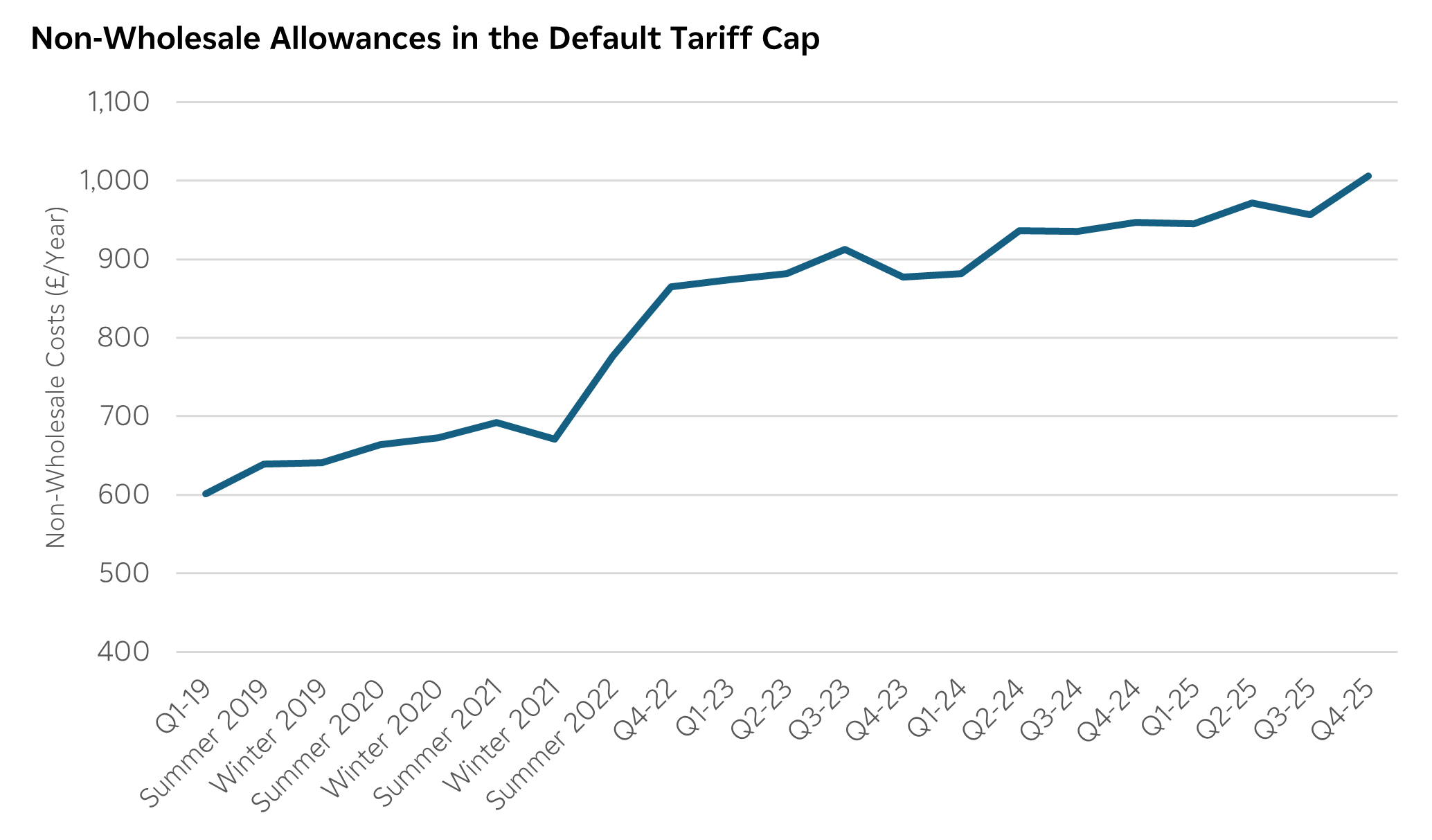

However, the wholesale price of energy is only half (38% based on the current Default Tariff Cap) of the story. The cost challenge is also increasingly about the non-wholesale costs that are recovered via our bills to, for example, support new investment in power and network projects, as well as social policies and supplier’s operational costs. These costs are growing fast – up 67% since the price cap was introduced in January 2019 based on Ofgem’s data as per the graph below. At EDF we are already predicting that the level of the price cap may rise by around another £100 next April, largely because of increases in non-wholesale costs.

Amidst the precarious balancing act of customer bills, reducing emissions and energy security, one thing remains clear - we need public buy in. That means bringing people on the journey with us, and as an industry doing our best to deliver a cost efficient and affordable energy system for the future.

Over the last few weeks, we’ve heard differing opinions on the trajectory of energy bills and what we should do about them. This blog sets out EDF’s view.

Will bills fall anytime soon?

Predicting energy prices can feel like a fool’s game. That said, governments and energy companies must attempt to look into the future to make policy decisions and secure the best deal for their customers.

That is what we have been trying to do at EDF. We have looked at how we expect wholesale and non-wholesale costs to evolve out to 2030, based on the current market and policy environment.

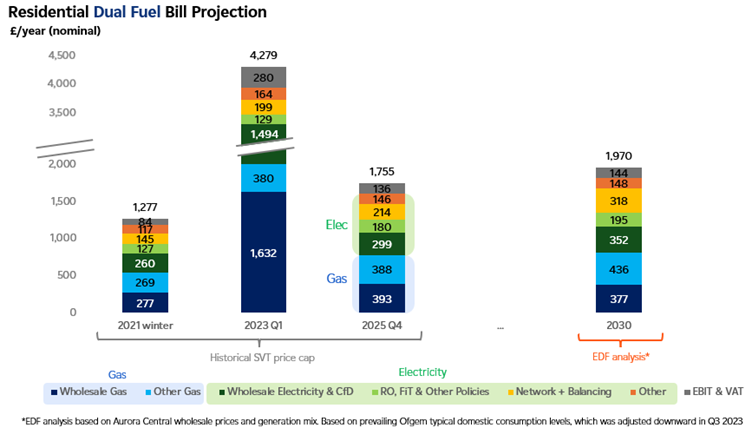

On current trends and without further intervention, our analysis, combined with data from Aurora, an independent energy consultancy, suggests that as things stand, bills are unlikely to fall this decade.

Wholesale gas prices and legacy policy costs should reduce in the coming years leading to some respite for customers, however, as we look further out, the introduction of new non-wholesale costs looks likely to quickly start offsetting these savings. On our projection, bills are likely to be around 12% higher in 2030 than they are today. As the chart below shows, this would leave bills around 54% above pre-crisis (winter 2021) levels, before the global gas price surge. Even after allowing for inflation over the period, this projection suggests that bills will remain elevated rather than returning to pre-crisis levels.

A key driver behind this is growing network charges. This is largely connected to the cost of financing additional network spend. Britain’s electricity network has historically been underfunded, and investment is needed to reinforce and modernise it.

As with any attempt to model the future, this is just one view. It’s therefore important to look at key sensitivities that could change this outlook.

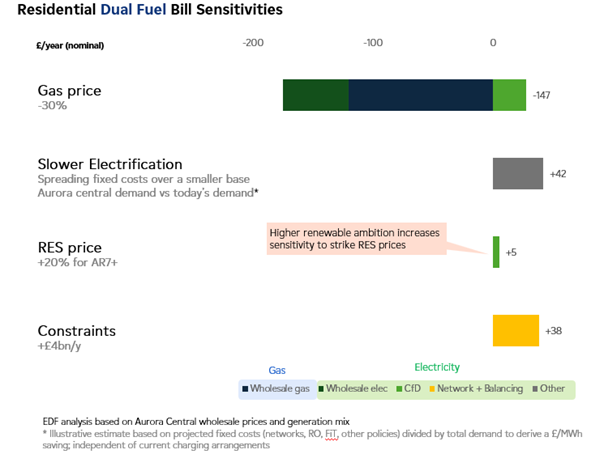

1. The price of gas

The biggest potential change would be lower gas prices. Gas prices around 30% lower than our reference scenario could reduce annual household energy bills by about £150, mainly through gas bills. Whilst lower gas prices would also lower electricity bills, the effect is softened over time as more power projects receive CfD top-up payments, reducing the net effect on bills.

2. The rate of electrification

Beyond gas prices, another key impact will be the rate of electrification. Most bill forecasts are predicated on the rapid electrification of the economy that helps to spread out the cost of new investment over a larger demand base.

Electrification can help keep electricity bills lower. Our modelling shows, subject to future charging arrangements (something Ofgem is currently looking at), electrification could save the equivalent of roughly £40 per household per year on average in 2030 by spreading largely fixed system costs over more demand.2

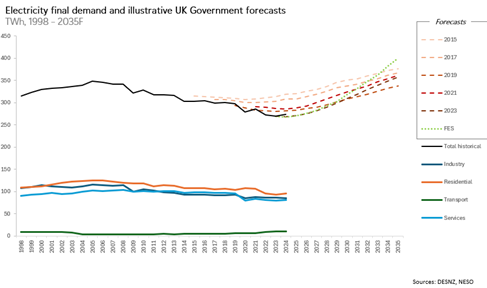

However, future levels of demand are currently highly uncertain. As a sector, we have been very wrong in the past about demand projections. Whilst there is a view that demand is increasing, we’ve actually seen electricity demand fall by 22% since its peak in 2005.

If rapid electrification doesn’t materialise, costs could end up significantly higher as we will not to be able to spread the cost of investment over a broader base. It would also mean that the spark gap (the difference in cost between electricity and gas) worsens and would make the very electrification that will lower bills even harder. A vicious cycle – and one that will only get worse post 2030 as we are hoping to see electrification accelerate.

3. The cost of new infrastructure and constraints

Finally, given the next decade will see a significant rollout of clean power projects, the full cost of these projects is also a key sensitivity. These costs will depend on the clearing price of CfD auction rounds, the trajectory of future wholesale prices and the pace and cost of network expansion. With global supply chains under pressure there is significant uncertainty around the future trajectory for renewables costs, even with the extension of CfD terms from 15 to 20 years.

For illustration, renewable strike prices 20% higher than baseline could add around £5 or more per customer per year.

Network constraints are another material risk. NESO’s scenarios show a wide range of potential constraint costs in 2030, reflecting differences in network and generation deployment, along with wholesale prices. Constraint costs £4 billion per year higher than baseline could increase electricity bills by roughly £40 per household.

So how do we stop bills rising further?

There is no silver bullet in this debate. No fix-all, easy solution which can tackle the cost of energy bills. Suppliers continue to operate on wafer thin margins (on average 1.47% for a domestic customer in 2024 according to Ofgem3) and struggle to attract investment. Our nation’s fiscal position means we must also think carefully about simply taking costs off bills and putting them elsewhere.

As a first step we need transparency. The Government has not published a Prices and Bills Report showing its overall outlook for bills since 20144. We must start from a shared understanding of how energy costs are likely to evolve to 2030 and beyond so a proper debate can be had on the costs of infrastructure and policy decisions.

From there, Government and the regulator will need to be creative and be willing to consider some broad and potentially challenging areas of action. Alongside important considerations around how energy costs are distributed across different households, we propose action in three areas:

A. Reduce the cost to serve

The cost to supply British consumers is unnecessarily high, its roughly double the cost in France (c. €45 per account in France v £100+ in GB). This is in part a result of our overly complex and rigid regulatory framework, which, for example, has significantly limited suppliers’ ability to recover debt, increasing costs for all. The cost of Ofgem itself has increased by 83% over the last 3 years, however, the consumer benefit derived for each pound spent has decreased by 41%5.

To reduce the costs to serve and bring down bills, we should:

- Deliver on the proposed Debt Relief Scheme as an important first step to help start to draw a line under the debt legacy of the energy crisis. By then broadening the scheme over time Ofgem could help ease the upward pressure record levels of bad debt is currently placing on bills.

- Commit to reducing the burden of energy regulation by 25% by 2030. While regulation is vital for consumer protection, a specific target to review all existing codes and licensing processes would force a mind-set shift to an outcomes-based approach and dramatically cut the cost to serve. This should include ensuring consumer protections are precise in supporting consumers they were intended to protect. Catch all or poorly targeted protections push up costs for all.

- Reform the smart meter roll-out by moving to a customer-pull model. By addressing inefficiencies in the current framework and implementing a ‘pull model’ we could save c. £200m/year across the industry. This requires immediate action as the costs of another new smart framework will be set from 2026 onwards.

- Establish a cross sector, government-led Priority Services Register. Creating a register of vulnerable people using data already held by Government would reduce the costs associated with identification and ensure available support is preserved for those most in need. In the interim, suppliers should be encouraged to verify consumer vulnerability upfront to get support to where it is most needed.

- Reset expectations around energy bills and debt. We need to foster a culture where all customers are encouraged to pay for their usage and help keep costs down for all. Key to this is ensuring suppliers have the tools and ability to recoup unpaid bills from those that can afford to pay and addressing regulatory drivers of debt such as the Change of Tenancy process. At the same time, we must ensure there is appropriate levels of financial support for those most in need (e.g. a reformed and expanded Warm Home discount/social tariff).

B. Electrify Britain

Bills will not fall in the long-term without electrification of underlying demand. This means rolling out products and services to help customers make the switch from fossil fuels and take greater control of their energy usage.

We can accelerate electrification by:

- Cutting VAT from electricity bills. While representing a new cost to the taxpayer, there is a case for removing VAT from household electricity bills as it would cut bills (by c. £40 a year) and narrow the gap between electricity and gas prices. Government should also consider cutting or removing the rate of VAT for public EV charging to better align it with home charging.

- Using the Warm Homes Plan to make access to electrification options fairer. Supplier obligations could be evolved to create a Warm Homes Obligation that focuses the delivery of heat pumps, solar PV and batteries to the most vulnerable so there is fairer access to the benefits of electrification. Typical customers could today save up to £260 per year by replacing their old gas boiler with a heat pump.

- Reforming the price cap in response to the move to Market-wide Half Hourly Settlement to ensure customers and suppliers have the right signals and incentives to use electricity more flexibly, helping to lower both their own costs and that of the entire systems.

- Changing the way we pay for legacy green subsidy schemes and network costs. The RO and FiT currently account for c. £120 of each household’s electricity bill. Moving these costs off electricity bills will reduce the ‘spark gap’ and accelerate electrification. While the current fiscal position may make it challenging to move such costs into general taxation, the costs could be securitised and paid back over a longer period to better match the lifetime of the investments they support. Given the rapid increases we are likely to see for network costs, spreading the costs over a longer period could also be applied to new price settlements within the network sector.

C. Optimise investment

Electrification and clean power will mean more secure and affordable energy for future generations. However, we have a responsibility to ensure investment is efficient and does not put too great a burden on today’s customers.

To drive better outcomes for consumers we should:

- Accelerate the development of a full Strategic Spatial Energy Plan for the energy sector to shape upcoming clean power and network procurement. This will need to include considering a range of electricity demand and supply scenarios that provide more certainty over what projects need to be built and where, but don’t lock consumers into costs that prove unnecessary. The plan should work hand in hand with the Reformed National Market, which will be essential to translate spatial priorities into efficient investment and dispatch decisions, harnessing the full power of market signals and private-sector delivery.

- Take action to lower the cost of capital of new generation, including through giving certainty on costs outside the control of generators, such as moving to fixed TNUoS costs for new projects. We estimate this action alone could save customers in the region of £12bn.6

- Ensure network price controls are agile at both transmission and distribution level. Given the uncertainty over levels of future demand we need to avoid locking in costs that don’t reflect the actual pace of electrification to ensure we minimise the risk for customers, whilst not obstructing the potential benefits. This will require supporting network investment that will resolve current constraints now but making effective use of uncertainty mechanisms regarding future investment that may or not be required based on future generation investment decisions. In addition, greater regulatory flexibility is needed in the provision of new transmission connections allowing competition to deliver faster, more innovative and lower cost developments.

- Link the UK ETS with the EU ETS to reduce carbon price volatility, helping to stabilise bills and paving the way for the removal of the Carbon Price Support scheme.

- Deal with constraint costs. As per our recent blog, the sector has a duty to consider swift and impactful interventions that can bring down constraint costs fast and save consumers money.

Conclusion

Many of our suggestions are not easy. Some will also take time to feed through to lower prices and bills. They should, however, be reinforcing and compounding. The more affordable we can help ensure electricity is today, the more likely it is that we can electrify at the rate required to keep bills down over the long-term and maximise the benefit of investment in new infrastructure.

There is only one way to deliver the energy transition – make electricity cheaper.

1 Default Tariff Cap as of Winter 2021 v November 2025

2 Delivering expected electrification-driven demand growth (~15 % by 2030) helps keep bills lower, by spreading around £30 billion/year of largely fixed system costs over more consumption - worth roughly £16/MWh on average or around £40 per 2.7MWh household. The extent to which any savings or costs are passed through to different customer groups will depend on future charging arrangements

3 Energy price cap benchmark review

4 Prices__Bills_report_2014.pdf

5 Comparing Ofgem’s annual expenditure v. annual consumer benefit achieved. Figures derived from Ofgem’s 22-23 and 24-25 Annual Reports

6 Figure is cumulative, in real terms and undiscounted

Related articles

Keeping a role for the market: how Reformed National Pricing can help deliver lower system costs

UK energy debt: why the crisis is deepening and what must change