UK energy debt: why the crisis is deepening and what must change

Energy affordability remains a real and pressing challenge for many households. While prices have come down from the peak of the energy crisis, the impact of the last few years is still being felt, with too many customers continuing to struggle with debt.

In this article Josh Buckland, Strategy & Policy Director at EDF and Keith Watson, Senior Manager in EDF’s Customers Policy and Regulation team, set out why tackling energy debt needs to be a priority, and how we can do it in a way that still continues to support those who need it most.

In this article:

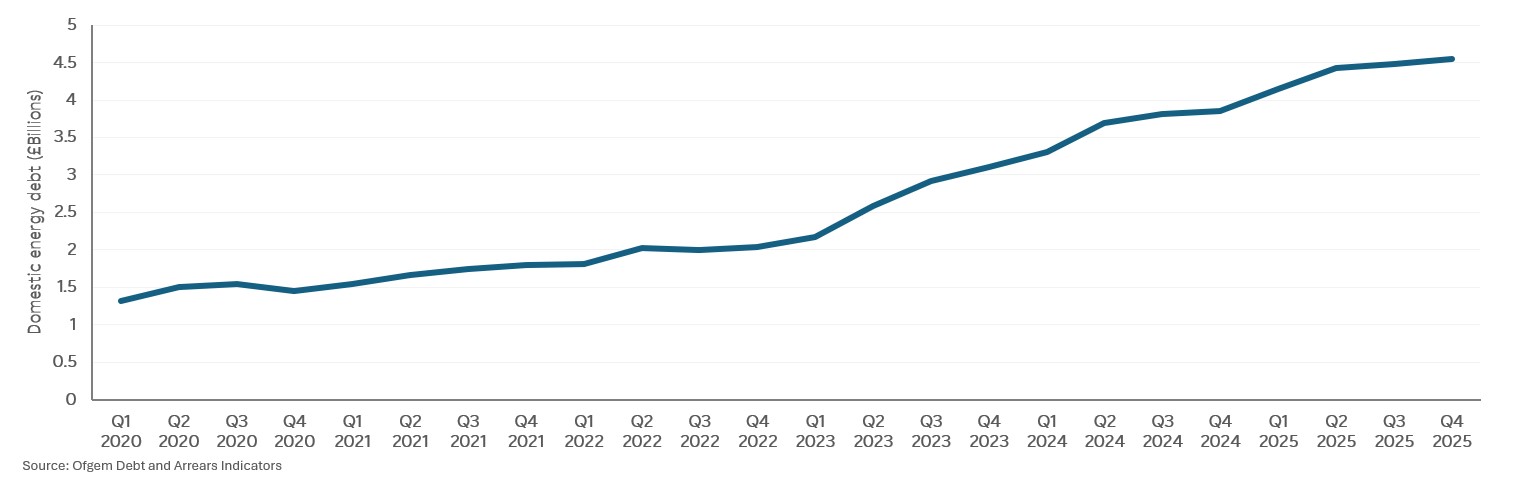

Energy debt levels in the UK are out of control. At the end of 2025 they reached a record £4.5 billion1, made up of around 3 million households who owe their suppliers an average of £1,500. A staggering 250% increase in the last five years. Industry estimates suggest this could reach £7 billion by the end of 20262.

It is not just consumers being driven into debt, but also those that are already behind on their energy bills falling further into debt. For example, more than half of EDF customers that are in debt today were in debt three years ago, but the value of this debt has more than doubled over the same period.

Worryingly this was not at all unexpected, the writing has been on the wall for some time. There are several contributing factors, notably high electricity prices caused by the conflict in Ukraine and the UK’s reliance on imported gas, the moratorium on the installation of prepayment (PPM) meters and wider cost of living pressures hitting the pockets of British consumers.

Despite Government action to reduce domestic bills from 1 April, the outlook is bleak, with the ongoing Middle East instability forecast to push up the price cap for an average customer by around £200 per annum from 1 July, according to EDF’s own energy price cap predictions.

Undoubtedly affordability remains the main cause of the escalating energy debt problem and one that has gone largely untreated now for far too long. However, there are other contributing factors that urgently need addressing.

In particular, the current regulatory framework has failed to keep pace with the problem. It has made it far too easy for consumers to get into debt and ever more difficult for suppliers to do anything about it. Regulatory protections designed for vulnerable consumers are, for example, shielding some customers who can and should pay, while unnecessarily prescriptive ‘catch-all’ requirements are also limiting suppliers’ ability to intervene before it is too late. Regulation is inadvertently contributing to a culture of non-payment because there are so few consequences for doing so.

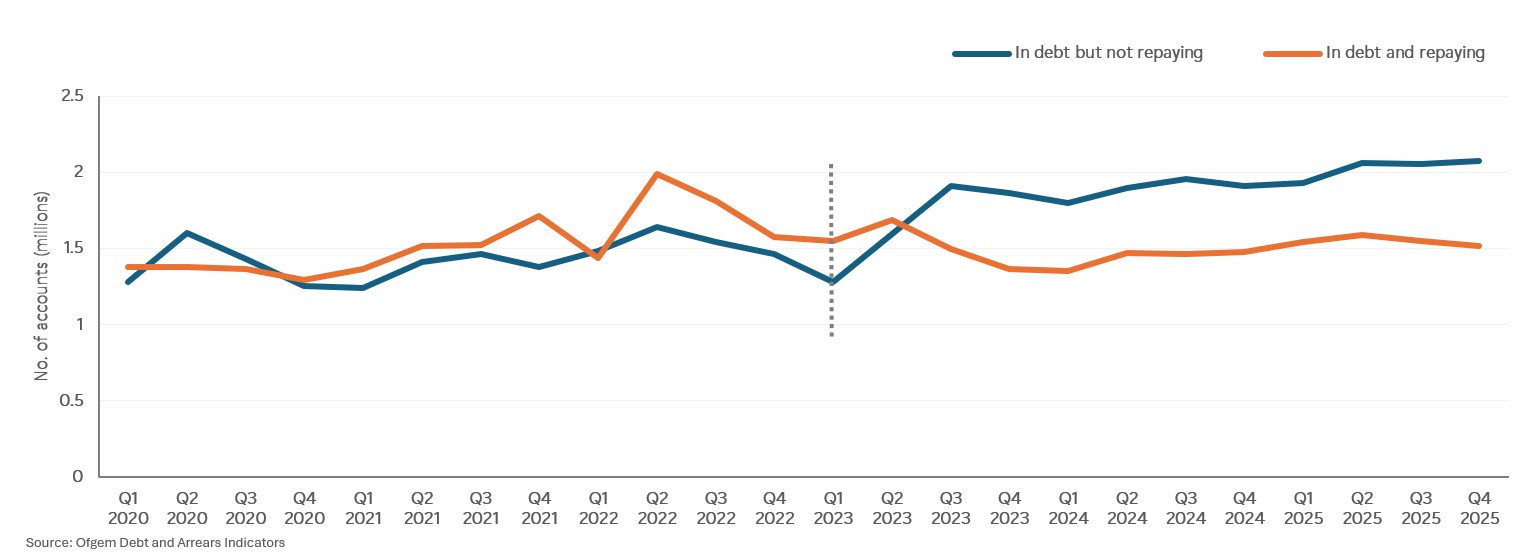

The moratorium on the installation of PPMs is perhaps the most obvious example of this. As shown in the graph below, there has in recent years been a big increase in the number of customers in debt not making repayments; this shift coincides with the point of the moratorium coming into effect towards the end of Q1 2023. Since then, this trend has continued, despite almost all suppliers now able to once again install PPMs for debt, albeit in a much more limited set of circumstances under Ofgem’s new regulatory framework. More concerning is the number of consumers who were reliably paying for their energy using a PPM who then switched to paying on receipt of a bill, that have subsequently stopped paying despite no identified change in their ability to pay. This alone for EDF accounts for c.£80 million of energy debt currently not in a repayment plan.

You may well ask, why does this matter to me, is this not just a problem for energy suppliers? Growing levels of debt, however, have a very real financial impact for us all – servicing this debt has a cost. Debt related costs today add around £60 to the typical annual energy bill. Industry experts have estimated that debt reaching £7bn this year would require a further £10-£15 per year to be added to energy bills3, driving up energy bills further and pushing more households into debt.

The objective must be to completely reset the debt landscape, regulation and culture that has persisted for the last five years by:

1. Better data-sharing, evidencing and verification

Energy suppliers are currently expected to accept all customer-provided information about vulnerability and personal circumstances without any evidence or verification, essentially operating on trust alone. This is unlike many other sectors, including government departments such as DWP which routinely verify eligibility for support before it is given. This lack of evidencing and verification allows some consumers to take refuge behind protections for which they are not eligible, constraining energy suppliers’ ability to recover debt and taking away from the additional support and services that suppliers offer to those who genuinely need it.

In the near-term there should be an expectation that information pertaining to a customer’s vulnerability or personal circumstances is verifiable and supported by evidence. This will ensure that those who genuinely need support and protections are rightly prioritised and that those who are not eligible and can pay, do.

In the longer-term, Government needs to accelerate plans to set up a cross-sector vulnerability and affordability register that makes better use of data sharing and the wealth of Government and industry data available. Not only would this better allow for the accurate identification of customers genuinely in need of additional protections, but this would also enable a far more sophisticated and fairer approach to the targeting of support.

2. An outcomes-based regulatory framework, involving smart Pay as you Go (PAYG) metering

The current regulatory framework is highly prescriptive with a ‘catch-all’ approach to debt. But debt is personal, complex and often driven by a mix of financial, behavioural and situational factors. Part of the problem here is that the current regulatory framework uses vulnerability as a proxy for affordability. While the two are often related, they are two distinct and separate challenges. For example, just because I have a child under the age of 2, that alone does not mean I cannot afford my energy bills.

In the last year alone the total amount of energy debt owed to EDF by customers with high affordability scores4 has increased by almost 10%, particularly among high affordability customers who have reported a vulnerability that means they are exempt from having a PPM (which has increased by 19%). Whereas the total amount of energy debt owed by customers with low affordability scores has remained largely unchanged.

We completely agree that the circumstances and vulnerabilities of some consumers, coupled with their inability to afford to keep the meter regularly topped up, would mean that it may not be safe for them to have a PPM. However, the current rule set is so broad that it effectively bans PPM for large parts of the population without any consideration of their wider circumstances.

A more outcomes-based approach where suppliers and customers must work together to assess whether a PPM is safe and practical that is informed by evidence and a consideration of the risks would lead to far better outcomes, rather than general bans that disincentivise engagement based purely on one personal characteristic. Such an approach must also once and for all draw a line between traditional PPM and newer Smart PAYG meters as these are fundamentally different propositions with completely different capabilities, such as easier budgeting, remote and auto top-ups and near real-time monitoring of where consumers may need support.

3. More ambitious and better-targeted support for those truly in need

As discussed above, for those genuinely in need of support, the root cause is very clear – many households simply cannot afford the energy that they need, especially in winter. The primary government support mechanism for these consumers is the £150 Warm Homes Discount (WHD) rebate, however the value of this has hardly changed since its inception 15 years ago despite energy prices increasing exponentially. For these households we need Government-led support to improve the ongoing affordability of energy. In combination with better data-sharing there is a real opportunity to introduce meaningful targeted support for these consumers, whether this be in the form of a social discount/tariff or otherwise.

We must also look to address the legacy debt that we have to contend with today. Ofgem has been in discussions with industry for nearly two years on the introduction of a Debt Relief Scheme (DRS), which would offer some relief to consumers and suppliers for debts accrued during the period where energy prices were at their highest. It is disappointing that this has so far continued to face repeated delays and dilution of its potential impact. Ofgem and Government must look to implement a more ambitious DRS with a broader, simpler structure that helps maximise the impact of this one-off intervention that could help get the industry and more importantly customers in need of support, back on track.

Conclusion: a necessary culture change

The UK energy market is at a crossroads. Without decisive action, rising debt will undermine the financial sustainability of suppliers, increase costs for customers who do pay their bills and weaken the investment the market needs.

A sustainable future requires:

- Better data sharing and verification to ensure protections reach those who truly need them

- A regulatory reset that prioritises outcomes over process

- Targeted affordability support to address the underlying issue and a bold approach to legacy debt

Only with these reforms can we shift away from the emerging culture of non payment and help start to build a fair, investible, and resilient energy market.

UK energy debt FAQs

What is the proposed Debt Relief Scheme?

The proposed Debt Relief Scheme is an Ofgem-backed plan intended to reduce some of the energy debt built up by households during the energy crisis. It has been discussed as a targeted intervention for customers who fell behind with bills and may struggle to repay, particularly where debt built up during the period of exceptionally high prices. It remains a proposed measure rather than a fully established, universal scheme.

What support does EDF offer customers who are struggling to pay?

EDF offers support, including payment plans, practical debt advice and signposting to external help for customers who are struggling with bills. There are wider support routes for customers in financial difficulty, depending on eligibility and individual circumstances.

Find out more:

- https://www.ofgem.gov.uk/data/debt-and-arrears-indicators

- https://www.energy-uk.org.uk/wp-content/uploads/2026/02/Energy-UK_Energy-Debt-Everyone-Pays_February-2026.pdf

- https://www.energy-uk.org.uk/wp-content/uploads/2026/02/Energy-UK_Energy-Debt-Everyone-Pays_February-2026.pdf

- Based on Credit Reference Agency data

Related articles

Keeping a role for the market: how Reformed National Pricing can help deliver lower system costs

The Warm Homes Plan: why faster delivery is critical for consumer bills and the country’s energy security