Myth vs reality: Do Virtual PPAs really shield buyers from balancing costs?

Corporate Power Purchase Agreements (CPPAs) enable corporate buyers to procure their power in a highly traceable manner from a renewable project. This helps them meet sustainability goals and hedge their energy costs out on a longer-term basis than they could otherwise do in the electricity market. Of course, this also helps renewable developers secure revenue certainty for their project, which, if it is a new asset, is needed to give the developer and its lenders the confidence to build the project.

Although there has been a significant effort across the industry to simplify CPPAs, many still find them complicated, especially for buyers who lack experience with CPPAs and may not have the right advisors to guide them through the process.

Physical CPPAs, in particular, have a reputation for being complex due to the amount of detail required in the contractual structure – such as concepts to do with forecasting renewable generation and the operations of the site, which are unfamiliar concepts compared to the provisions of a typical supply agreement.

On the other hand, Virtual CPPAs tend to avoid the need for any of that and are therefore viewed as a much simpler contract, which is attractive to many. They do come with the complication of some complex financial accounting practices, but the setup at least is certainly simpler for corporate buyers.

EDF regularly talks to corporate buyers, generators and their advisors on the latest trends and market drivers. Through those discussions, we also hear that Virtual CPPAs are popular for corporate buyers as they are cheaper than Physical CPPAs because they avoid shaping and balancing fees.

A cheaper CPPA sounds like a great solution for corporate buyers, but is it really true?

What is the difference between Virtual vs Physical CPPAs?

Physical CPPAs

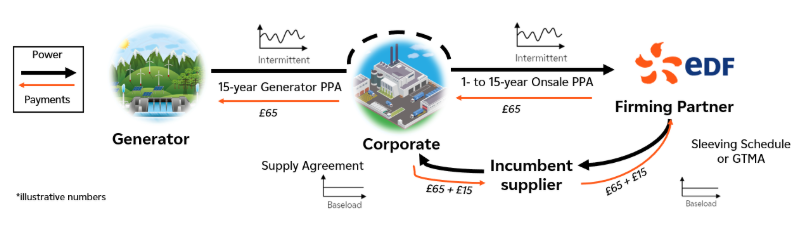

Physical CPPAs are the most common structure in GB, often taking the form of a Direct Physical CPPA. Under this structure, the corporate buyer contracts directly with the renewable generator to purchase their intermittent power for a fixed price. As the corporate buyer is unable to accept physical delivery of the power, they will seek a firming partner like EDF to buy the power off them for the same fixed price. The firming partner then converts the intermittent power into baseload blocks and provides this power back to the corporate through its supply agreement, via the incumbent supplier. For providing this service, the firming partner charges “firming fees”, often termed “sleeving fees” or “shaping and balancing fees”.

Importantly, these firming fees do add to the overall costs that a corporate pays for the power and must be considered carefully in the decisions that a buyer makes when entering into a CPPA.

On the face of it, it is certainly a complex structure, but it is a common path for many GB firming partners/suppliers, and with the right people on board, it’s not as daunting as it may appear.

Virtual CPPAs

Virtual CPPAs are on the rise and becoming increasingly popular in the market. Their increasing popularity comes from two main reasons:

1) Their simplicity

2) They avoid a corporate having to pay for shaping and balancing fees

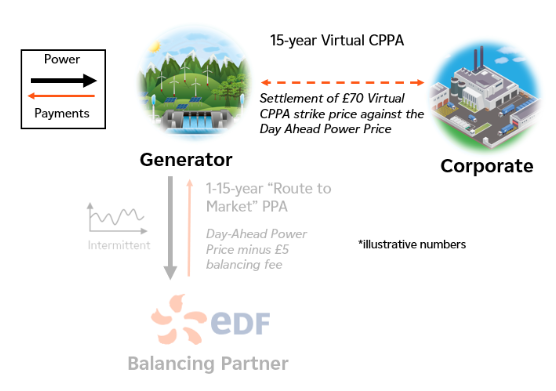

Contractually, they are the simpler model for CPPAs in GB, as shown in the diagram below. The corporate buyer only has to enter into one agreement - the Virtual CPPA with the generator - which essentially pays the generator a fixed price for its power output. As the name suggests, this is a purely Virtual (financial) arrangement, as no physical power is given in exchange for this payment. Instead, the generator essentially pays the corporate the variable Day-Ahead market power price in exchange for receiving the fixed power price. This means that when the Day-Ahead power price is lower than the fixed price set in the Virtual CPPA, the corporate buyer “tops up” the generator to the fixed price, and when the Day-Ahead power price is higher than the fixed price, the generator “pays back” the corporate buyer to equal the fixed price. In doing so, this acts somewhat like a hedge for the corporate buyer. This is in the same way as the government’s CfD agreements are operated.

What is shaping and balancing?

Shaping and balancing, collectively termed “firming”, are the actions that need to be taken to convert intermittent power from a renewable generator into baseload blocks of power. These blocks are much more traceable than the intermittent power, making them ideal for then selling to the market, other suppliers, or sleeving into corporate supply agreements.

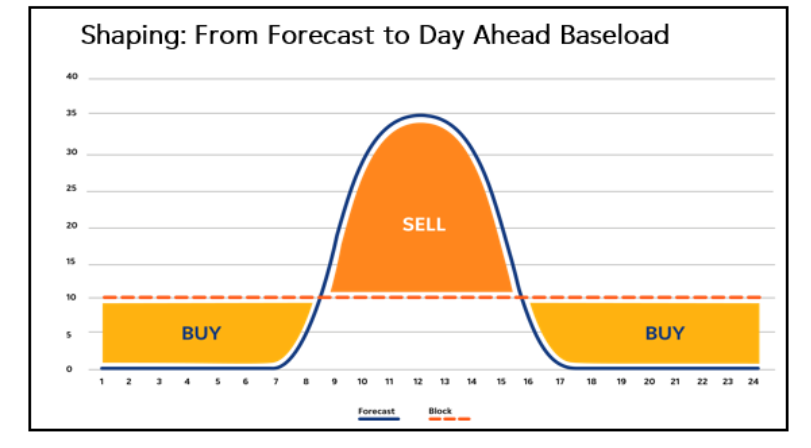

Shaping

Shaping is the act of converting a forecasted generation output into baseload blocks at the Day-Ahead stage for delivery (be it to the market or to a corporate buyer), and in doing so creating short positions that have to be bought back (when generation is lower than the baseload block) and excess positions that have to be sold back (when generation is above the baseload block). For CPPAs, when firming fees are fully fixed, this will be done when the fees are agreed and locked in, hedging the position of those buys and sells.

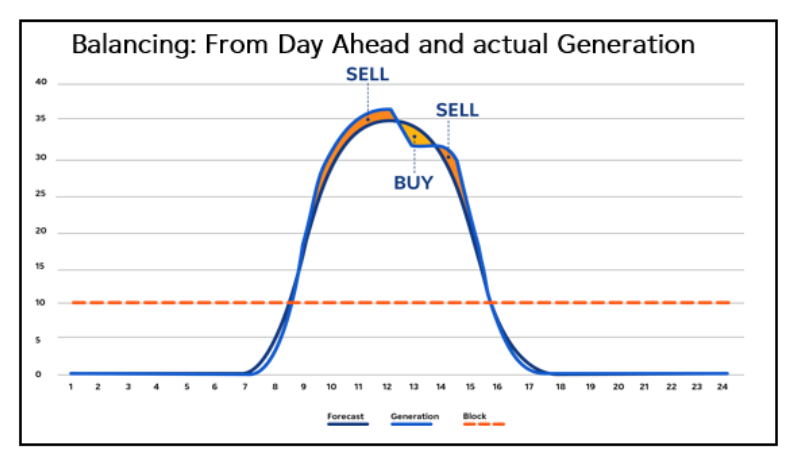

Balancing

With shaping converting the power from a long-term forecast into baseload blocks at the Day-Ahead stage, balancing then picks up the variance from Day-Ahead to actual generation. It is the act of correcting any errors in an asset’s forecast at the Day-Ahead stage of delivery to the actual outturn of the generation. Costs arise when there are differences in forecasted generation to what is actually generated, meaning the party responsible for balancing is exposed to buying back any shortfall in the forecasted position or having to sell excess power that wasn’t forecasted previously.

If a Virtual CPPA doesn’t involve the delivery of power, does that mean balancing and shaping costs wouldn’t apply?

In short, no, you still pay balancing and shaping costs as a corporate buyer.

But let us explain. Balancing and shaping costs are intrinsically tied to all power generation and consumption; there is just no avoiding it. It is just a matter of transparency and awareness, and understanding who is taking on those risks and costs.

Focusing on CPPAs, under a Physical CPPA, the firming party takes on the shaping and balancing risk, and therefore charges “Firming Fees” or “Shaping and Balancing” fees to the corporate buyer for providing that service. That means that on the corporate buyers’ bills and statements, there will be a clear charge for those costs. It also means that the corporate buyer can negotiate and structure those fees to better suit their business’s risk profile – a concept we will cover in another blog. The point being, the fees are known to the buyer.

Under a Virtual CPPA, how the corporate buyer still incurs shaping and balancing fees is less obvious, but nevertheless, those costs are there. Starting with balancing, under a virtual CPPA structure, the renewable generator needs to sell its power in the Day-Ahead market in order to settle its CPPA price, and by doing so, will sell its power to a balancing partner like EDF in what is commonly termed a “Route to Market PPA”. Under this Route to Market PPA, the balancing partner assumes balancing risk, which, as explained above, means they have to buy any shortfall in generation or sell any excess generation to the market between the Day-Ahead stage and actual outturn.

As this typically nets as a cost to the balancing partner, it charges a balancing fee to the generator, who receives the Day-Ahead market price minus a balancing fee. In the knowledge of this fee, the renewable generator will inflate the Virtual CPPA price it offers to the corporate buyers to pass this cost on, meaning even in a Virtual CPPA, it is actually the corporate buyer who inadvertently pays for balancing.

The corporate buyers also face shaping costs under a Virtual CPPA due to the mismatch between the output of the renewable generator and their own corporate electricity consumption. If a corporate buyer aligns the Virtual CPPA size with its annual consumption (i.e. a Virtual CPPA with a 50 GWh generator for a corporate that buys 50 GWh of power per year) then there will be times when the generator is producing more than the corporate’s electricity demand and times when it is producing less, and whilst that doesn’t impact anything physically it does impact the financial settlement materially.

When the renewable generator is producing a large amount of power, it is likely that other renewable generators around the country are doing the same, which drives down the Day-Ahead power price as renewables have zero marginal costs to run. Under a Virtual CPPA, the corporate buyer would have to pay a top-up to the renewable generator during these periods, which results in a relatively high cost due to the amount of power being generated.

When the renewable generator is producing small amounts of power, it is likely that the other renewable generators in the country are doing the same, driving up the Day-Ahead power price, with conventional generators having to be turned on to meet demand. This would see the corporate buyer getting a relatively small gain from getting paid back to the Virtual CPPA price from the Day-Ahead price, but for a small amount of power.

The netting of this small gain and high cost is the “Shaping Fee” that would be incurred under a Physical CPPA.

The table below summarises where balancing and shaping costs sit under both CPPA structures.

Firming Costs | Where are they in a Physical CPPA? | Where are they in a Virtual CPPA? |

Balancing | Paid by the corporate buyer. Priced by the Firming Party in a transparent manner. | Paid by the corporate buyer. Priced in by the renewable generator, often not transparently |

Shaping | Paid by the corporate buyer. Priced by the Firming Party in a transparent manner. | Paid by the corporate buyer. Not transparent without the ability to be fixed, but picked up by the corporate buyer due to the netting of Virtual CPPA settlements and their supply agreement |

Conclusion

CPPAs are a brilliant way for corporates to buy green power and hedge their electricity costs, whilst supporting real renewable generation in GB.

They can be complex, but with the right partners and advisors, businesses can make informed decisions that will stand them in good stead for the years to come.

At EDF, we often hear that many corporate buyers are entering into Virtual CPPAs to avoid the costs of shaping and balancing that they would be exposed to in Physical CPPAs. While we encourage corporates to hedge their electricity costs and support renewable energy, we think it is important that these choices are informed by a complete understanding of the facts.

It’s a common misconception that Virtual CPPAs avoid firming costs. In reality, all CPPA structures involve balancing and shaping costs as they are an integral part of the electricity market. Those risks cannot go away, so corporate buyers must understand where these risks sit and how they are being “priced in” to their contract.

If your business is ready to embark on a CPPA journey, EDF can help you navigate the options and unlock long-term value from clean energy procurement.

Related articles

AR8: What Should Developers, Investors and Energy Buyers Expect from the UK's Next CfD Auction?

UK electricity demand: why it matters for business competitiveness and what must change