The price of abundance: Solar trends in GB’s sunniest season

As we settle into Autumn, it’s clear that Summer 2025 left a powerful legacy when it comes to solar generation.

The season delivered record solar generation across Great Britain, reaching a new summer record of 13.8TWh - surpassing the previous high of 10.4TWh. While this surge has been a win for solar generators, it also marked a historic peak in solar cannibalisation, a phenomenon that’s reshaping how we value renewable energy.

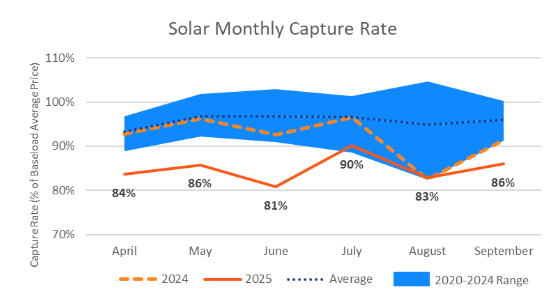

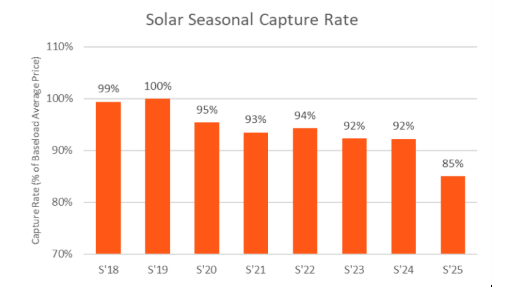

Over the summer, solar captured just 85% of baseload Day Ahead prices, significantly below the market average, highlighting the growing impact of solar saturation on pricing dynamics.

What is solar cannibalisation?

When solar output peaks across the grid, it saturates supply and drives down electricity prices - especially during hours of sunlight. This phenomenon, known as solar cannibalisation, means solar generators often earn less than the market average.

To quantify it, we compare:

- The average Day Ahead power price (a simple average across a given period),

- With the solar-weighted price, which reflects how much solar is generated during each hour.

This summer, we’ve seen a huge amount of solar generation, driven by the increased build of new solar in Great Britain, along with a particularly sunny summer, which meant that solar captured just 85% of the baseload Day Ahead price.

This means solar generation won't be worth as much as you might expect when you look at baseload forward power prices - and it has been a lot less valuable, over Summer 2025. Ironically, abundant sunshine can drastically erode solar’s market value.

Why does this happen?

Power prices are shaped by the balance of supply and demand. Consumers are only willing to pay so much for electricity, which creates a demand curve. On the other side, generators offer electricity based on how much it costs them to produce it - this is called their Short Run Marginal Cost (SRMC) - which forms the supply curve. The market price at any moment is where those two curves meet.

When demand goes up, prices rise. When more cheap electricity (like solar) is available, prices fall. Solar, with its ultra-low production cost, floods the grid during sunny spells. Because many solar farms generate simultaneously, the market becomes oversupplied with cheap energy - reducing the need for higher-cost generators and pulling prices down.

Think of it like a farmers’ market where everyone brings tomatoes at once: the more supply, the lower the price.

What made Summer 2025 so extreme?

Solar capture rates for Summer 2025 have been significantly lower as a percentage of baseload prices than any other recent summer season. Several factors have amplified cannibalisation this year:

- More solar capacity: GB now boasts over 17GW of solar, from utility-scale solar farms to rooftop panels.

- Cross-border solar imports: Countries like Germany and the Netherlands ramped up solar exports to GB via interconnectors like BritNed.

- Weather patterns: Prolonged sunny, mild conditions boosted solar output while curbing electricity demand - creating the perfect storm for price suppression.

What does this mean for developers, generators and offtakers?

The recent spike in solar cannibalisation - driven in part by the unusually sunny summer in Great Britain -is a clear signal of shifting dynamics in the energy market. While it’s too early to predict long-term trends, the implications for PPA offtakers, developers, and generators are already taking shape.

For PPA offtakers: Higher cannibalisation means increased shaping costs. This high cannibalisation is a timely reminder to PPA offtakers to make sure they are adequately forecasting this effect and managing their risks so they can continue to offer developers and generators competitive PPAs going forwards. While this uptick was anticipated and already factored into our cost forecasts, it doesn’t currently warrant a change in the PPA pricing offered by EDF.

For developers and generators: Partnering with experienced offtakers who understand and can manage this volatility ensures more stable returns and long-term project viability. As the market evolves, collaboration and transparency will be critical to sustaining growth and resilience across the sector.

This trend underscores the importance of robust forecasting and risk management. Offtakers must stay ahead of market shifts to continue offering competitive PPAs. Volatility in earnings is part and parcel of renewable contracts, and navigating these fluctuations is where offtakers add real value.

To keep you in the loop, we’ll be publishing monthly updates on how capture rates evolve - watch this space!