COVID-19 – The impact on battery storage revenues

We know that COVID-19 has had a significant impact on national demand, falling by as much as 20 percent versus forecast. We also know that this fall in demand has had a significant impact on National Grid’s ability to balance the system. As a result, we've seen the introduction of ODFM to allow National Grid to turn down embedded generation, or increase load, and we've seen the introduction of GC0143 which, as a last resort, allows the ESO to instruct a DNO to disconnect embedded generators. But what impact has this drop in demand had on battery storage revenues?

Has the fall-off in demand led to a more benign market, which is bad news for storage assets, or has lower demand resulted in increased turn-down of subsidised renewables assets and actually increased revenues for storage assets?

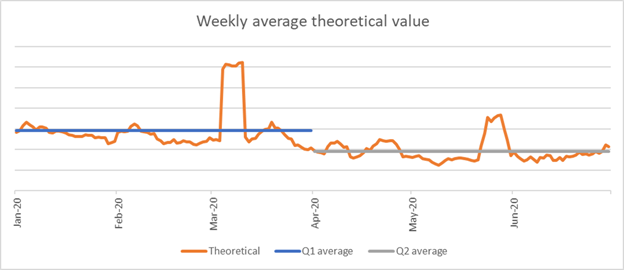

The chart below shows the theoretical revenue for a non-BM asset that's available 24/7. It's first being optimised through the day-ahead auction, and then re-optimised within-day using a combination of spot prices and cashout. The value itself would only be achievable if we had a perfect forecast of spot prices and cashout (i.e. it’s completely unachievable without a DeLorean!!!), but it’s a useful measure as things like real time performance are removed from the equation.

What we can see from the chart is that whilst there may have been a few ‘good’ weeks since demand reduced due to COVID-19, average theoretical traded (non-BM) revenues are about a third lower in Q2 than they were in Q1 (not taking into account seasonality or the revenue secured in other markets such as ODFM and FFR).

However, there may be some light at the end of the tunnel. To the right of the chart we can see that since the start of June the theoretical value has been slowly but quite steadily increasing. This increase coincides with restrictions gradually being lifted, demand picking up and the country moving slowly moving back towards where it was before this all happened. As with anything market related, there is no guarantee of what will happen in the future. A spike in COVID-19 cases could lead to further restrictions which in turn could pull battery revenues downwards or upwards again. But we expect this revenue stream to continue to improve as the economy returns to normal, or the ‘new normal’, anyway.

So, in summary, the COVID-19 impact could have be quite significant IF you were relying on a single revenue stream like wholesale markets and had failed to secure a floor price with your Optimiser. Luckily at EDF we have had a few offsets that have neutralised this short term fall off in just one of our revenue streams:

- We continue to be successful in securing well priced FFR contracts for low inertia periods;

- We are active in ODFM for non-BM units;

- We have continued to improve our forecasting capabilities under COVID-19 which has increased revenues from our NIV chasing strategy.

Our ability, and strategy, to target multiple revenue streams means that as traded revenues have dropped off, our focus has pivoted and we have offset much of the reduction in traded revenue. So whilst the pie shrank, our slice was bigger!